Most responsible businesses today know that it is not if but when they become a victim of a cyber attack.

But no matter how much you invest in cyber security, your business isn’t truly safe from cyber-attacks until you’ve got proper cyber insurance.

Cyber insurance can help your business to cover the costs, expenses and liabilities that arise from data breaches, data extortion, business interruption and other cyber security threats.

Understanding what exactly cyber insurance is, everything it covers and why it’s so important could protect your business from serious cyber crimes.

Cyber insurance is fast-becoming the most essential of insurance products and helps to protect businesses from the costs and liabilities of cyber threats. No two businesses are the same, which is why good insurance providers offer tailored cyber insurance packages that suit the needs of each individual client. Depending upon your needs, your cyber insurance can protect your business from the costs, expenses and liabilities that arise from:

Cyber insurance can come in a huge variety of packages, and it’s always important to check what your policy covers before you sign. Consider the wide range of cyber threats that your business is vulnerable to and make sure that your policy covers them all.

Cyber insurance is the only way to make sure that your business is fully protected from the risk of a cyber attack. Cybercrime cases and data breaches are increasingly becoming a major threat to businesses in every industry, which is why more and more CFOs are choosing to protect themselves with cyber insurance.

To understand why cyber insurance matters, let’s consider some of the scenarios that could occur if (when) your business suffers a cyber attack:

In each of these cases, the only way to protect your business from potentially bank-breaking costs and liabilities is through cyber insurance. No matter how much you invest in information security systems, where humans are involved, there are opportunities for manipulation and deception: all it takes is a memory stick of confidential data dropped in a public place.

Investing in reliable, transparent cyber insurance – tailored for you by La Playa – can help your business shore up its defences against inevitable incoming cyber attacks. We partner with insurers who understand the risks specific to tech and digital industries, so you can benefit from expert advice to make smart decisions for your business.

The benefits of working with La Playa on your cyber insurance include:

The popularity of cyber insurance has skyrocketed since the introduction of GDPR in the EU and CCPA In the US, and the pandemic has only intensified the risk. Strict data regulations across the globe mean that companies have greater obligations to protect their data than ever before – and with these obligations come very real risks.

Cyber insurance isn’t a replacement for cyber security: as a modern business operating in a digital marketplace, protecting confidential data is the obligation of all decision-makers, and indeed a governance issue for boards. But, despite most businesses investing heavily in cyber defences, successful cyber attacks still happen every day.

Cyber insurance can provide businesses with an extra level of security and peace of mind in the face of the ever-changing landscape of digital security. You can’t always stay one step ahead of cybercriminals, but you can shore up your defences just in case.

Make sure you get the most out of your cyber insurance with our three top tips for choosing a comprehensive cyber package that gives genuine value:

La Playa is backed by leading global technology insurers and our specialist team will design an insurance program for your organisation that provides comprehensive protection at sensible prices.

Flexible and efficient, we combine personal service with expert advice – the perfect partner to guide you through the complex and ever-changing risks your enterprise will face.

La Playa’s insurance experts offer advice you can trust from people who understand your business, with:

Experience best of breed insurance policies, the La Playa way.

La Playa is a specialist insurance broker offering an intelligent approach to insurance for clients in the creative, digital and tech industries as well as for high-net-worth individuals.

Contact us today to find out more about how we can help you to protect you and your business.

2020 was hardly a banner year for most of us. The COVID-19 pandemic reminded us all that predicting the future is rarely anything other than a lost cause.

But it did also arguably shape the future in an unprecedented way as it caused a major shift in all sectors towards remote working and digitisation.

How is the insurance sector going to cope in a year that will be just as eventful? Let’s have a look at some trends we see taking shape over the next 12 months.

Insurance has always run on hard and soft cycles, with a soft market meaning lower premiums for customers and more profitable investments and underwriting results for insurers.

However, thanks to a number of natural disasters and climate change related major losses and not helped by COVID-19 inflicting record losses on insurers across the globe, the current hardening trend in the insurance market in 2021 looks set to continue to toughen even further.

What this means for customers is that insurance will become harder to come by, and insurers will start to raise rates to reflect the major losses that have occurred in recent years.

With this potential new avenue to navigate, it’s more important than ever to connect with the right advice. A key strategy for controlling premiums is keeping claims to a minimum – which means a good regime of risk management, supported by advice and expertise from your insurance broker.

With money tight across the board, there will likely be an increased demand for more flexible, usage-based insurance products.

However, these products are likely to be rather basic and designed for those who can’t afford fixed premiums.

Artificial intelligence and automation have been seeping into the insurance sector for years now but could 2021 be the year it finally starts to dominate? The consensus is that that technology will be used primarily from a customer experience perspective, personalising and simplifying the claims process.

However, it’s in the processing of data that the really exciting applications lie. This could mean more accurate premium calculation, of course, but also more accurate identification of emerging risks and faster claims. In the coming years, even the underwriting process may be completely automated.

It’s only natural that, in the wake of a pandemic, people would start to care a little more about their health.

This means insurers will respond by bolstering their traditional medical covers with more advanced and specific products and services.

Lockdown and other pandemic-related restrictions have catalysed a greater demand for digital transactions and that includes insurance policies.

Going forward, this shift towards digital means insurers are going to have to stop being reactive and start being proactive, as the market becomes more about preventing losses than providing compensation for them.

The insurers that stand to benefit the most are the more innovative specialist insurers who have doubled down on their niche (or niches) and have a greater reserve of more specific data to work with.

With machine learning at the helm, predictive analytics is going to be the wave of the future and it is the companies willing to ride that wave that are going to reap the biggest rewards.

With the world moving online at an alarming rate, cybersecurity is becoming a more significant threat every day.

That means we’ll be seeing more businesses in 2021 investing in more specific cyber insurance and insurers will be doubling down on providing complete transparency to their customers.

Overall, it seems that it’s the demand for more tailored products that will prove the foundations for insurance in 2021.

Pandemic insurance, for example, is an itch that still needs to be scratched. For those in the events industries and arts, cancellation policies are going to be a primary concern too. And as well as policy wordings being designed for particular niches, these will need to be supported with advice from an expert with specialist experience within that sector.

In all, 2021 is likely to be a year of consolidation, more than expansion for the insurance sector. It’s going to be a year that hopefully outshines its beleaguered predecessor. Here’s hoping, anyway.

Image: Jirapong Manustrong / Shutterstock.com

With the COVID-19 pandemic dominating headlines across the globe now for the best part of the last year, our health has never been more at the forefront of our minds. In recent months, meanwhile, the stories have pivoted away (somewhat) from the lockdowns and infection rates towards something a little more hopeful – the vaccines that will get us all out of this mess.

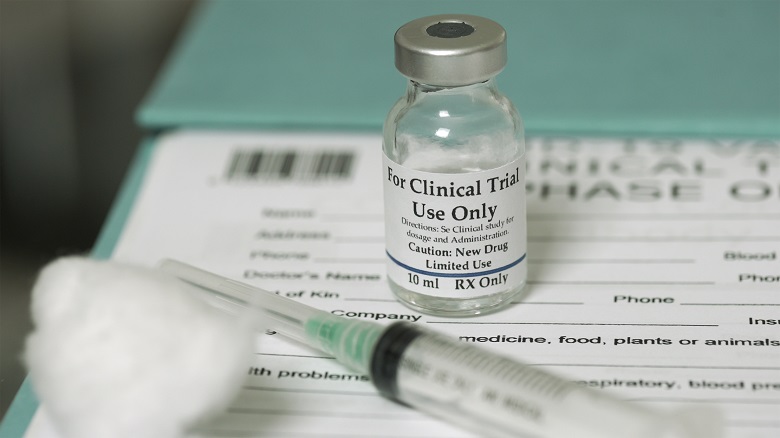

These vaccines have been developed at lightning speed by some of the most innovative scientists and pharmaceutical companies in the world and the pace of vaccine development has relied on a multitude of new clinical trials.

Clinical trials have been a part of medical science for decades now and some of the greatest advances in medicine couldn’t have been made without them. There are, however, always going to be risks associated with such trials. If a participant has an adverse reaction to the as-yet untested medicine, for example, what kind of liability does the pharmaceutical company behind the trial have for the health and safety of the patient?

Volunteers are always protected by a high-spec framework of risk management, of course, but there’s always an element of risk. This is why it’s imperative all institutions that undertake clinical trials have specialist clinical trials liability insurance in place.

With new EU regulations set to change the landscape further, with which the UK is likely to align, and the pandemic moving the goalposts every step of the way, clinical trials insurance has never been a more vital piece of the puzzle.

Negligent harm – Harm caused during a clinical trial as a direct result of alleged negligence.

Non-negligent harm – Harm that occurs as a result of the trial but with no specifically definable cause. Policy wording here should always work in accordance with the guidelines for regulators in each territory.

In the majority of cases, it will be the sponsor of the clinical trial that arranges the insurance and this can be anyone from a pharmaceutical company to a University or a biotech company. In short, if you are an institution that uses clinical trials to further your development then it’s a cover you can’t operate without. You should also sort out insurance ASAP, as you often need the certificate of insurance to hand when you submit to the ethics committee.

Clinical trials were once solely about drug development. However, today the landscape has changed. Modern clinical trials might involve testing new equipment or procedures and these trials come with their own risks that need to be covered by more specific lines of cover.

Say, for example, that a software error occurs when uploading medical imaging software. This error then means the patient has to have multiple images retaken, causing added emotional and physical distress. Years ago, this wouldn’t have been covered but insurers have had to adapt to changing technologies and changing trends.

We also live in an increasingly litigious world, where medical lawsuits are distressingly common and can lead to reputational damage and financial loss too. Then there are the latest EU regulations on clinical trials (from 2019) which affect both the limit of cover stipulated and the way the insurance is structured.

Any broker offering a specialist life science policy should be able to arrange clinical trials insurance, either as an extension of existing cover or a separate policy. If it’s part of a broader insurance portfolio then it’s more likely to cover every base.

All specialist brokers should have genuine expertise in life science insurance, be agile enough to respond rapidly, understand country-specific requirements and have foreign and domestic capabilities.

Ultimately, it’s up to each trial sponsor to ensure they have an open and honest partnership with their insurance broker. In a fast-moving, competitive environment. it’s always the human beings at the centre of the trial that should come first. Without these volunteers taking their own risk, there would be no trial.

Image: Scott Cornell / Shutterstock.com

COVID might have sullied the water somewhat for the creative industries, with the last six months throwing hurdle-after-hurdle at those who create everything from video content to books and TV – particularly those whose primary income stream is based in the live arena.

With such uncertainty constantly nibbling at our collective heels, there’s never been a worse time to be caught out with an intentional and unwarranted tort such as libel, plagiarism, or invasion of privacy.

That’s why, in a nutshell, any company that creates, produces or markets creative content of any kind really needs media liability insurance.

Your company is probably already insured under a commercial general liability (CGL) policy, which covers claims made against your business that result from an offence included in the definition of personal injury.

However, CGL excludes libel and slander, not to mention several other infringements that media and creative businesses might often be accused of. So, without media liability insurance they would have no coverage.

For example, if an online magazine published a negative review of a local establishment and stated that the health standards were below par and the establishment were to sue that magazine, the magazine would only be covered if they had media liability insurance.

The same would also be true if a movie production company was being sued by a music publisher for using a song in their movie that they didn’t obtain the license for.

These are both examples where, without media liability insurance, the offended parties would have no legal costs coverage.

It’s a type of insurance typically offered by insurers that deals specifically or primarily with the creative industries and so has a greater well of knowledge to pull from and act in the best interests of their clients.

It’s technically a type of errors and omissions insurance purchased by businesses that create and provide content, to protect them from a variety of torts relating to the media.

This can include, but is not restricted to, the following:

What kinds of media liability insurance do specialist insurance brokers cover?

You’ll find most brokers willing to offer media liability coverage, but for those in more specific sectors, it might be worth looking a step further at even more niche insurance that caters directly to the areas you’ll be operating in.

Are you a social media influencer, for example, that often discusses products or other influencers on your various channels? Have you ever paused to consider what would happen if you got your facts wrong and ended up accidentally spreading false information that left you open to a lawsuit?

Or are you often signing deals with brands that ask you to promote products and have wondered what might happen if you neglect to declare your interest to your audience? These could be covered by a bespoke personal media profile insurance plan that is tailored around the legal needs of bloggers, vloggers, and influencers.

Whichever field you fall into, if your business is in media then there is almost guaranteed to be a more specific insurance policy available that focuses on your exact needs – rather than everything under the sun.

Sometimes, a more focused hand is more effective than a jack-of-all-trades and in such an uncertain world, sometimes a skilled and focused hand could make all the difference.

For those businesses in the endlessly dynamic advertising and marketing sector, it makes sense to focus resources primarily on what makes that industry so important – the innovation, the passion and the creativity.

But the world of advertising is also one that often finds itself walking a legal tightrope and if you’re not best-placed to prepare for these legal consequences (and the costs they can incur) then you could end up in hot water. And in this current uncertain climate, cool waters are always appreciated.

Advertising often deals with intellectual property by design and in that game, there is great potential for legal liability and serious claims. That’s why legal risk management is so crucial in the sector and should not be neglected as a minor consideration.

Managing risk in advertising and marketing means constantly asking yourself the following questions:

If you’re working with any kind of creative content, whether it be words, pictures, logos and particularly the brand name, it all constitutes intellectual property and to use it legally, you must either own the rights to it yourself or have contractual permission to use it.

So, before submitting any content to your clients, always ensure you are 100% legally allowed to use every piece of creative in the campaign.

Creative ownership is also true when considering work done by freelancers and sub-contractors because while there is the assumption that all work created in the course of a campaign is owned by the employer, if there is no written agreement then the third-parties could potentially contest that the work you’ve handed into your client contains their intellectual property. To avoid this, ensure all contracts written up with third parties contain very clear working parameters.

If you’ve been asked to sign an NDA or confidentiality agreement prior to a pitch then all information you receive before the pitch should be kept under lock and key.

Indeed, even if there is no NDA involved, if the information you receive is quite obviously supposed to be confidential then if you share this information and the potential client experiences a loss as a result, they might have a legitimate claim against you.

Any breach of the Data Protection Act of 1998 constitutes a criminal offence and in a post-GDPR world, the lines in the sand have been drawn with even greater clarity.

If you’re planning on marketing directly to a client’s customer base you must ensure you obtain a warranty and indemnity from the client that ensures the contact information was obtained legally. Otherwise, you could end up being stuck with a fine of up to £500,000.

Job titles might not always reflect an individual’s employment status and it’s possible for some individuals to be treated as self-employed for tax purposes, but as an employee for insurance purposes.

Businesses must ensure they have put in place employer’s liability insurance and given the blurred line that often occurs between the employed and self-employed. This is particularly common in the creative and media industries, businesses would be wise to take out policies that cover both equally, preferably from a specialist insurance broker.

Comparative advertising is as old as advertising itself and is used today by everyone from video game console manufacturers to political parties.

However, it’s a potentially dicey area to get involved in as if you put a foot wrong you could land your client in hot water.

Your marketing must not mislead the audience and can’t be seen to be piggy-backing on the reputation of a client competitor. It’s a tactic that has been used by Pepsi and Burger King in the past – but just wouldn’t float in this day and age.

Of course, there are dozens of other considerations to make and potential risks to juggle and as the industry continues to evolve there will be dozens more to come.

Although most marketing and advertising agencies set out to stick to the basic rules of advertising (be legal, be honest, be prepared, and be respectful), things can go awry unintentionally.

That’s why it’s so important to work with a specialist insurance adviser who really understands your risks, and to have a secure specialist insurance policy in your back pocket just in case you slip up.

Let’s be honest, it happens to the best of us.

The coronavirus crisis has changed a lot of things for a lot of people. It’s also resulted in a significant amount of global economic uncertainty. Venture capitalists do not thrive on uncertainty, they thrive on calculated risks and transparent long-term outlooks.

But despite the tumultuous impact of COVID-19, can there still be a positive road ahead for VCs looking to expand their portfolios in a complicated climate?

At its beating heart, venture capitalism is all about investing in innovators and perhaps the only positive thing about a crisis is that its wake often necessitates innovation.

VCs must continue to innovate in kind if they hope to survive the ramifications of coronavirus. But what does the post-COVID immediate future of venture capital look like?

Keeping it close – With a heightened real and perceived risk internationally and difficulties to travel, many VCs will likely choose to invest closer to home in the coming months.

The strong win out – Virus or no virus, the best companies will always draw the most interest regardless of where they’re located.

So, whilst it might be more convenient to shop closer to home, so to speak, and there may be a funding pause for a while, video conferencing can fill in the gaps when it comes to facilitating parts of the due diligence process.

Healthcare in, entertainment and travel out – With healthcare very much on the minds of everyone right now, healthcare tech is going to start looking a lot more tempting for many VCs. On the other hand, businesses focused on areas, such as travel and entertainment (particularly live music), are going to take a backseat for a while.

Virtual working – Investments in technologies that facilitate virtual engagement are likely to become more attractive to investors as more of us are working from home and going digital.

The new normal – Businesses are going to need to adapt to the ‘new normal’ of social distancing whether they like it or not and that’s going to result in some major economic and behavioural changes.

VCs are going to have to be vigilant in examining the residual impact of this new status quo if they want to invest wisely and gain some decent returns.

Most tech-based businesses are 24/7 operations that are both global and borderless and as such, they are constantly being exposed to new potential risks and liabilities – often in unfamiliar places.

As the law struggles to keep pace with technology, specialist insurance can provide a legitimate safety net if you fall foul of changing legislation.

It’s important to know that all companies you invest in are properly insured – to ringfence the risk in your investments, La Playa can help with your due diligence, identifying the business risk, providing an Enterprise Risk Report and recommending a programme of bespoke insurance and risk management.

We can also help with your business insurance. While your commercial appetite for risk may be higher than average, you’ll want to know your internal business risk is nailed down most efficiently and effectively.

One thing we’ve learned in a post-COVID world is that nothing should be taken for granted and that legislation is constantly in flux.

In such a climate, don’t you want to eliminate the maximum possible risk – and to know your insurance is being taken care of by somebody that speaks your language?

That’s why specialist science and technology insurance is something that any VC with at least one finger in the tech pie should specify in contracts.

Who wants a jack-of-all-trades behind the wheel when the goalposts are constantly being moved from beneath our feet?

If you love modern art, you’ll love these great tips from R L Sparks and Charlotte Perman, Private Collection curators for Martin Lawrence Galleries (MLG) in New York. And after you purchase your new pieces, don’t forget to protect their value with the right insurance cover!

1. Condition is king.

We cannot overstate this. A great lesson and example would be to review the sale of Superman #1. A printing of this comic categorised as a Grade 9.0 sold for $2.16 million in November 2011. An edition categorized as an 8.5 sold in March 2010 for $1.5 million. The difference between an 8.5 grading an a 9.0 was described to us as a “small fold in the cover”…a $616,000 fold to be precise! The same applies to art. The best condition works equate to the best values.

2. Don’t disregard prints.

After all Andy Warhol was a printmaker and not renowned for his painting skills! Some of the most important works in art history are prints – Picasso’s deeply personal Vollard suite, Chagall’s stunning lithographic series Daphnes and Chloe, and Lichtenstein’s The Melody Haunts My Reverie, all of which are housed in museum collections. Don’t get tied up in the “cult of canvas”!

3. Good buys can still be found under $10,000.

Take Takashi Murakami for example, the so-called Andy Warhol of the 21st Century whose artwork hangs in the Museum of Modern Art. Though his paintings and sculptures sell for millions of dollars, his hand-signed limited edition prints are available to purchase for under $10,000, with many under $5000. These prints are exquisitely designed, employing some of the most high-tech practices in printmaking today – embossed backgrounds, layers of gloss inks and utterly unique style.

4. Buy for love, but only under $10,000.

We both agree that collecting should be fun and owning art should be enjoyable. If you can afford to decorate with art up to a price point of $10,000 then we support that, but beyond that we recommend making a more educated purchase that will hold its value in years to come. There is a strong likelihood that you will be able to marry the two, acquiring a piece you enjoy living with that will also secure your initial investment, if not improve upon it.

5. Buy to hold.

The media is rife with stories of people ‘flipping’ small purchases for high returns but these are the exception to the rule. True collectors buy to hold and by doing so see the best return on their investment. In truth one should be looking to buy with a view to living with the art for a minimum of 5 years. A speculator and a collector are two very different things!

About Sparks & Perman

R.L. Sparks and Charlotte Perman manage Private Collections for the Martin Lawrence Galleries. With almost 40 years’ history, MLG likely has the largest privately held inventory of any gallery or collector, amounting to some 10,000+ units of art, all owned, none on consignment. Sparks and Charlotte specialize in the rarest works from within the collection by the most significant artists of the 20th Century, including Andy Warhol, Pablo Picasso, Roy Lichtenstein, Marc Chagall, Sam Francis, Salvador Dali, Alexander Calder and Keith Haring.

“Jane Byde is Head of Fine Art at La Playa Limited, a boutique specialist insurance brokerage with offices in Cambridge, London and New York. Her clients include private and corporate art and jewellery collectors, galleries and dealers.”

Tell us about your work

As a broker, my job is to listen and understand clients’ needs, assess the products available and advise as appropriate, making sure the client is doing everything they should to make it work for them. We are not employed by insurance companies, nor are we lawyers, so cannot advise on the minutiae of what will be decided in a court of law if anything goes wrong. Ultimately, it is about managing expectations, being a go-between for clients and underwriters and explaining why the cover costs what it does.

What led you to your current role? Are you yourself passionate about art?

I have always been an art lover, visiting museums and galleries from a very early age, so it was natural to study Art History at undergraduate and Museum Studies at postgraduate level. After university I worked for six months in galleries on Cork Street, before ending up in hospitality management, gaining a diploma from the Wines & Spirits Education Trust. In the course of my work, I met many people in the insurance industry who encouraged me to become a broker because attention to client needs is critical for both roles.

I found a role in marine insurance with a top-three insurance brokerage and studied alongside my job for three years to obtain my ACII, which is the equivalent of an insurance ‘degree’. Another five years later an opportunity opened up in the Fine Art sector and I jumped at the chance as the role allowed me to progress my career, but utilises my knowledge base and passion for art.

How can you make your insurance work for you?

Many people are understandably frustrated when what they feel is a legitimate claim is declined or the value paid out below what they expect. Frequently though, the reasons for insurance not performing as you expect are simple and result from poor housekeeping which could easily be avoided.

Having an up-to-date valuation of your treasures is critical for getting the most out of your insurance. Most of the contentious claims we see are where an assured has little evidence of the value they are claiming for.

A private insurance policy is usually based on Agreed Value which means that in case of a loss, insurers will pay up to the value of the item as listed in the inventory, which is based on the latest professional valuation of your collection. Insurers expect valuations to be done every 3-5 years. Some insurers will pay an increase to the inventory price to match the current Market Value if prices have gone up since the valuation, but this is often capped at a level which may be insufficient for certain artists and jewellery in particular.

Most auction houses will do a simple low-cost appraisal of your art and antiques whilst professional appraisal firms will do a thorough one for somewhat more. There are many services available and it is not essential to use one of the big three auction houses.

What if you have lots of items to insure? It seems like this could become a bit of a time drain for serious collectors!

All policies covering art and antiques will have a limit at which all items under this value are lumped in together as a “total unspecified value”. Each item exceeding this value needs to be listed on the inventory or schedule, which your valuer will provide. Standard High Net Worth homeowner’s policies usually have an unspecified article limit of £10-15,000, whilst a dedicated art collection insurance policy will normally have a much higher limit of £25-30,000 per item. This means you will only need to list your significant pieces and not every last silver salt shaker.

Couldn’t a wealth manager take care of all of that?

Most wealth managers are not specialists in insurance and in all but the most straightforward cases will involve an insurance broker in your case anyway. In the High Net Worth sector in particular, time-poor clients frequently become highly reliant on their trusted advisers to organise their affairs on their behalf. Whilst strong relationships are an important part of keeping your affairs in good shape, don’t be afraid to question them, talk to other people or set the challenge of proving they are interrogating your coverage correctly. Finally, make sure they are speaking to a specialist broker who is trained and experienced in the appropriate sector.

I have had my insurance policy for years and it seems to suit me fine. Why should I look elsewhere?

Insurance moves with the times just like everything else. Risks that weren’t covered or were costly years ago may be feasible now and vice versa; some elements you have taken for granted may no longer be covered depending on your circumstances or the claims experience of the industry. Take time to consider one or two alternative insurance providers as far in advance of your renewal date as you can, ideally a month or so ahead.

What is the single highest value item you have insured?

A few years ago I helped insure a single cut diamond for display at a well-known London department store, with an insured value of £50,000,000. As you can imagine, the security measures surrounding the item would have fit well into a Mission Impossible script! Individual paintings or antiques are rarely insured on a stand-alone basis other than for exhibition or transit purposes as economies of scale and risk-spread normally mean a collection is best insured as a whole.

What’s the one piece of advice you’d give to someone looking for insurance?Insurance is built on trust. Underwriters rely on the information we provide them with and if a claim arises from a risk they weren’t informed about, that trust can be broken and problems paying claims may arise. Of course unexpected accidents happen and that’s what insurance is for, but being honest and upfront, disclosing everything can about the risk you are looking to insure is a good start.

Allow your broker to visit your home or spend time chatting to them on the phone and they will do much of the work for you. One of the benefits of using a Lloyd’s Broker over an online tool or a volume broker, is that we still speak face to face with underwriters about your circumstances. We look them in the eye and develop relationships to win their trust, just as we do with you as clients. It is a powerful communication tool which helps us get the best terms for you, and differentiates us as a quality specialist broker.

Finally, if you cut corners by not disclosing critical details, your upfront premium could be wrong and this in itself could be problematic if you have a claim, due to underinsurance. Your insurer may be within their rights to decline to pay all or part of the value because you didn’t disclose facts relevant to the risk.

Can you give some examples of these critical details that may affect a claim?

Not advising that you kept certain artworks stored in a basement could be one. Or perhaps failing to disclose that you only have security cameras pointing to the front of the house and not the back, or that you don’t have locks on the windows of your ground floor apartment.

What if your circumstances change?

Admin is tedious but necessary. Ensuring the correct individuals and locations are listed on your insurance policy helps avoid disappointment. On a good quality homeowner’s insurance policy, your art collections should be covered anywhere in the world including in transit, if securely and adequately packed. If you move home or purchase an additional property and move artwork there you need to inform your insurance company, because the security measures will be different. Sometimes, such changes are for the better and occasionally will improve your premium, for instance if you move away from a flood-prone area or transfer your most valuable painting from the ground floor of a townhouse to a second floor apartment in a gated and concierge-monitored block.

What happens to property insurance if a policy owner dies?

You may not be aware that property insurance does not operate like a life insurance policy; there is no automatic beneficiary and the policy does not automatically transfer to heirs upon death of the original owner. Making sure your heirs and trusted advisers are aware of the insurances you have in place, and potentially listing heirs as joint-assureds, is a sound idea for ensuring protection of homes and collections in the event of your death.

Let’s say Mrs Smith, a widow of ten years, passes away leaving her home and the art collection inside to her son. He holds on to the property as he is considering moving into it with his own family, but does not think to transfer the insurance policy into his own name. A few months later a burst pipe damages some of the furniture and art work. In this case the homeowners’ insurance would be unlikely to pay any restoration or replacement costs for the art work except possibly on an “ex-gratia” goodwill basis, as the new property owner is not listed on the contract of insurance.

What can you do if your (ex) spouse is the policy holder, and they refuse to disclose valuations?

If your (ex) spouse is refusing to add your new property to the insurance policy as above or will not provide a copy of the current valuation, there’s not much you can do without instructing your lawyer to pursue them specifically on this point. It is much simpler and no doubt significantly cheaper to get another valuation done and obtain your own policy for the items you are keeping within the divorce agreement.

What is the most unusual insurance claim you’ve ever encountered?

Thankfully fine art claims are rare because collectors generally take good care of their valued possessions, but we did once have a claim for artwork shipped with an obvious dent and tyre marks on the packaging, from having been run over, presumably by the shipper’s own van! The worst claim we have seen was a damaged old master canvas torn by a rolled up magazine flying at it, during a row. In the wider Private Client team I work with we have seen a Porsche roll into a pond when the handbrake was left off and a pheasant-rearing shed on a smallholding burn down, killing several thousand tiny occupants.

How have technological advancements affected the responsibility placed on the individual?

Previous generations relied on paper ledgers, hand-written receipts or even a handshake from their dealer as proof of purchase. In this day and age, lack of attention to records for valuable purchases and failure to ensure your evidence is backed up, just doesn’t cut it. Technology has streamlined our record-keeping via use of email, retailer’s databases and the advent of cloud storage, meaning that even storing files exclusively on a home computer is an unnecessary risk to take. Most valuers or appraisers will provide an e-copy inventory with photographs as well as a hard copy. It sounds obvious but you can even take your own pictures and store them digitally. If you receive paper receipts from a purchase, snap a picture of the invoice on your smart phone or scan it in using local facilities. Ensure your broker has a copy of your inventory and that you also have it saved somewhere secure, preferably in a secure online storage facility such as iCloud or Dropbox.

Why would anyone hack the NHS? Why would anyone hack your business?

But you should be thinking “when”, not “if” now.

Cyber security is a pressing management issue – and with new GDPR data laws, the potential cost of an attack or breach is spiralling.

.jpg)

TIP: make sure your Cyber Risks Insurance covers Crime: financial protection for theft of money and fraud, including phishing scams, electronic wire transfer fraud, telephone hacking and social engineering.

If you don’t already have Cyber Risks Insurance, talk to us as a matter of urgency. Our advice is always free and without obligation.

6 BASES TO COVER IN PREP FOR A HACK OR DATA BREACH

The majority of small businesses have had their digital defences breached in the past year. It’s vital to protect your intellectual property, business information and customer data against online theft and exploitation. Read on for a basic checklist on preparing for an cyber attack:

1. Risk assessment on security and the “what ifs” for your business

2. Security controls: maintain, regularly update and stress-test them

3. Incident response plan: create and share it, and make sure you have the right professional help at the ready

4. External back up systems in place

5. Educate and train all staff to reduce human error

6. Cyber Risks Insurance – make sure it covers Crime:

If you don’t yet have Cyber Risks Insurance, just try quantifying the potential costs of a hack or breach. Even with well-trained teams and systems in place but it may still happen to you. With data breaches, hacks, ransomware and human error – you need to make sure you’re covered and have a team of experts on hand to resolve the issue.

If you do have Cyber Risks Insurance, check your covers and limits are still adequate, and that you have access to emergency response teams. Make sure your policy covers Crime: financial protection for theft of money and fraud, including phishing scams, electronic wire transfer fraud, telephone hacking and social engineering.

To talk it through, or if you need connections to professional services in these areas, don’t hesitate to get in touch.

Jane Byde – Head of Fine Art:

E: jane.byde@laplayapartners.com

La Playa: Insurance with Intelligence

People like you like us. Passionate. Discerning. Independent.

Those of us privileged with owning fine art and instruments have a responsibility to protect them for future generations.

These good practices will help protect your art and instruments, your bank balance, and – to some extent – your legacy…

1. Valuation: changing trends in the art, antiques and jewelry markets mean that the replacement value is constantly shifting – and premiums may need adjustment (up or down). If you’re not aware of the value of your assets (or if it’s not documented), you could find yourself significantly under-insured. After the trauma of a theft, the last thing you need is the worry of a difficult negotiation over the value of each piece. Regular valuation, inventory appraisal and photographic records will all help.

2. Security: better protection can mean lower premiums; insurers recognize the extra care taken. If your jewelry collection is valued over $25,000, consider installing a home-safe (and for collections over $50,000, a second safe connected to the alarm system). We can advise on security marking, and anti-intruder installations that won’t compromise the integrity of your home.

3. Insurance: make sure you have a personalized policy fine-tuned for your specific needs and lifestyle. These need not be prohibitively expensive; indeed fine art and instruments normally cost less to insure than standard contents – especially if you have evidence of taking extra steps to protect your belongings. If you’re still buying ‘standard’ homeowners’ policies, you might be in for some surprises when you make a claim.

4. Documentation: it’s important to keep safely:

• Appraisals

• Historical records

• Insurance paperwork

• Repair paperwork

This can really help with claim resolutions and the repair or replacement process.

646 665 7737

646 665 7737